Background

In 2015, the EU introduced changes to the EU VAT directive and its implementing regulation which inter alia

1. Contained a unified definition of electronic services, and

2. Introduced new rules on how the supply of electronic services should be taxed.

At the time, the concept of digital distribution platforms was already well established, and a considerable amount of electronic services were sold through such platforms. Examples include Apple’s App Store and Google’s Play Store. These types of online platforms are characterised by the relative ease with which suppliers can offer their electronic services for sale, usually to non-taxable persons (consumers). The online platform traditionally collects revenue through commission fees paid by the underlying suppliers, calculated as a percentage of the sale price towards the end-customer.

B2C sales of electronic services over online platforms by small suppliers inherit a tendency to remain unreported as these types of transactions are difficult for tax authorities to monitor and control. To prevent non-reporting of these transactions, the EU introduced a presumption by which the online platform is deemed to be the supplier of the electronic service sold to the end customer (Art. 9a of the European VAT Implementing Regulation in connection with Article 28 the EU VAT Directive, in Germany implemented in Sec. 3 Para. 11a German VAT Act).

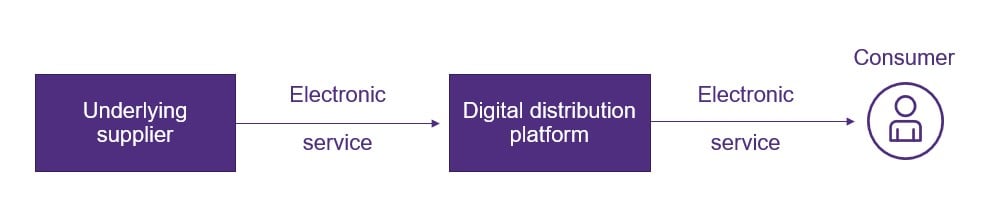

A simplified visualization of said presumption looks as follows:

Source: Grant Thornton Germany

As a consequence, the reporting liability of VAT from the individual suppliers shifts to the online platform itself. This means that the online platform is obliged to report VAT on the entire price of the electronic service, not only on the commission fee charged towards the underlying supplier. In turn, the underlying supplier is considered to make a sale of the same service to the online platform itself; the price of this service being the final price paid by the consumer less the commission charged by the online platform. For the digital distribution platform, because of the special place of supply rules on B2C sales of electronic services, this also means that additional VAT liabilities could be incurred in any country where an end-customer has its domicile or habitual residence.

The presumption which shifts the reporting liability can be broken, however only in cases where the underlying supplier is explicitly indicated as the supplier of the electronic service by the online platform and when this is reflected in the contractual arrangements between the parties. As will be shown, breaking this presumption can be hard given how digital distribution platforms are currently operated.

The case at hand

OnlyFans is an online platform where content creators offer electronic services to consumers. Fenix markets OnlyFans itself and provides associated services to the content creators, such as the payment system. The end customers pay through either subscriptions or one-off payments. Fenix collects as commission 20 percent of the price which the end customer pays, forwarding the rest of the payment to the content creator (= supplier).

In 2020, the British Tax Authority (HMRC) sent assessments for VAT due to Fenix. HMRC was of the opinion that Fenix should have reported VAT on the entire sales price charged by the content creators utilizing the online platform. In essence, they argued that the presumption described above was applicable in this case – which would make Fenix the deemed supplier of the electronic services and as such liable for reporting VAT on the entire amount paid by the end customers. Fenix on the other hand had only reported VAT on the commissions which they charged the individual content creators, on the basis that they, in their opinion, only provided a commissionaire service to the content creators utilizing the OnlyFans platform.

In front of the UK national court, Fenix inter alia argued that implementing such a presumption was contrary to the powers which are given to the EU. The national court decided to stay the proceedings and put forth the question regarding the legality of the presumption to the ECJ.

Verdict of the ECJ

In short, the ECJ ruled that the presumption in Article 9a of the EU VAT Implementing Regulation was not contrary to EU law. Because the presumption was not broken in this case, HMRC was right in deeming Fenix as the supplier of the electronic services sold to the end customers. This also means that the content creators using OnlyFans are considered to supply their electronic services to Fenix / OnlyFans and not to the end customers. This constitutes a major change as the taxation of electronic services differs between B2B and B2C transactions. This is further complicated by many different factors, such as the domicile of the underlying supplier and whether they are liable to be VAT registered at all. To conclude, the ruling imposes significant VAT liabilities and costs on Fenix and potential VAT refunds for the content creators.

When motivating the ruling, the ECJ clarified that the presumption regarding the taxation of electronic services sold through marketplaces was merely an implementation of the already existent rules which can deem any intermediary as the supplier of goods or services for VAT purposes. This opens the possibility of applying a wide array of previous case law to the presumption established for electronic services. In particular, the ECJ mentions the following regarding the contractual relationship between the digital distribution platform and the underlying supplier:

“Where a taxable person, who takes part in the supply of a service by electronic means, by operating, for example, an online social network platform, has the power to authorise the supply of that service, or to charge for it, or to lay down the general terms and conditions of such a supply, that taxable person may unilaterally define essential elements relating to the supply, namely the provision of that service and the time at which it will take place, or the conditions under which the consideration will be payable, or the rules forming the general framework of that service. In such circumstances and having regard to the economic and commercial reality reflected by them, the taxable person must be regarded as being the supplier of services, pursuant to Article 28 of the VAT Directive.”

Our recommendations

The present ruling present adds significant certainty in the VAT treatment of electronic services supplied through digital distribution platforms. However, given how digital distribution platforms are currently operated, the VAT implications are likely not positive for the operators. The characteristics that make digital distribution platforms so successful: Accessibility, security, and ease of use for the end customers – factors that make the latter feel like they are interacting with a large and trusted online platform rather than small individual suppliers – are also likely to have the consequence that digital distribution platforms to a greater extent will be deemed as suppliers of electronic services sold on their platforms, rather than just a middleman.

Many digital distribution platforms are likely to already be set up in such a way that is compliant with the presumption and deemed supplier rules, with some even offering it as an advantage to the underlying suppliers who can avoid complicated reporting or additional registration requirements. Companies operating platforms where services are offered are strongly advised to check for potential VAT risks in light of the above.

This topic is accompanied by potential reporting obligations under the Platforms Tax Transparency Act introduced as per 1 January 2023 (Plattformen-Steuertransparenzgesetz (PStTG).